Let's Get Started

To spur economic activity within an Opportunity Zone, a significant tax incentive is available for private, long-term investment in these designated areas. Anyone who is interested in maximizing their capital gains, or profits from the sale of an asset, is encouraged to consider the option of reinvesting these dollars into a Qualified Opportunity Fund, in exchange for considerable federal capital gains tax reductions. Investors with realized capital gains have 180 days from the date of the sale or exchange to invest their gains into a Qualified Opportunity Fund (QOF). The QOF then needs to place 90% of the funds into qualified opportunity zone property or business within six months.

Incentive Options:

- Investors can defer paying taxes on the original capital gain until they dispose of the investment or until 2026.

- If the investor holds the investment for at least five years, they will have to pay 10% less taxes on the original capital gain.

- If the investor holds the investment for at least 10 years, they will not have to pay any capital gains tax on their opportunity zone investment.

- Investors can defer paying taxes on the original capital gain until they dispose of the investment or until 2026.

- If the investor holds the investment for at least five years, they will have to pay 10% less taxes on the original capital gain.

- If the investor holds the investment for at least 10 years, they will not have to pay any capital gains tax on their opportunity zone investment.

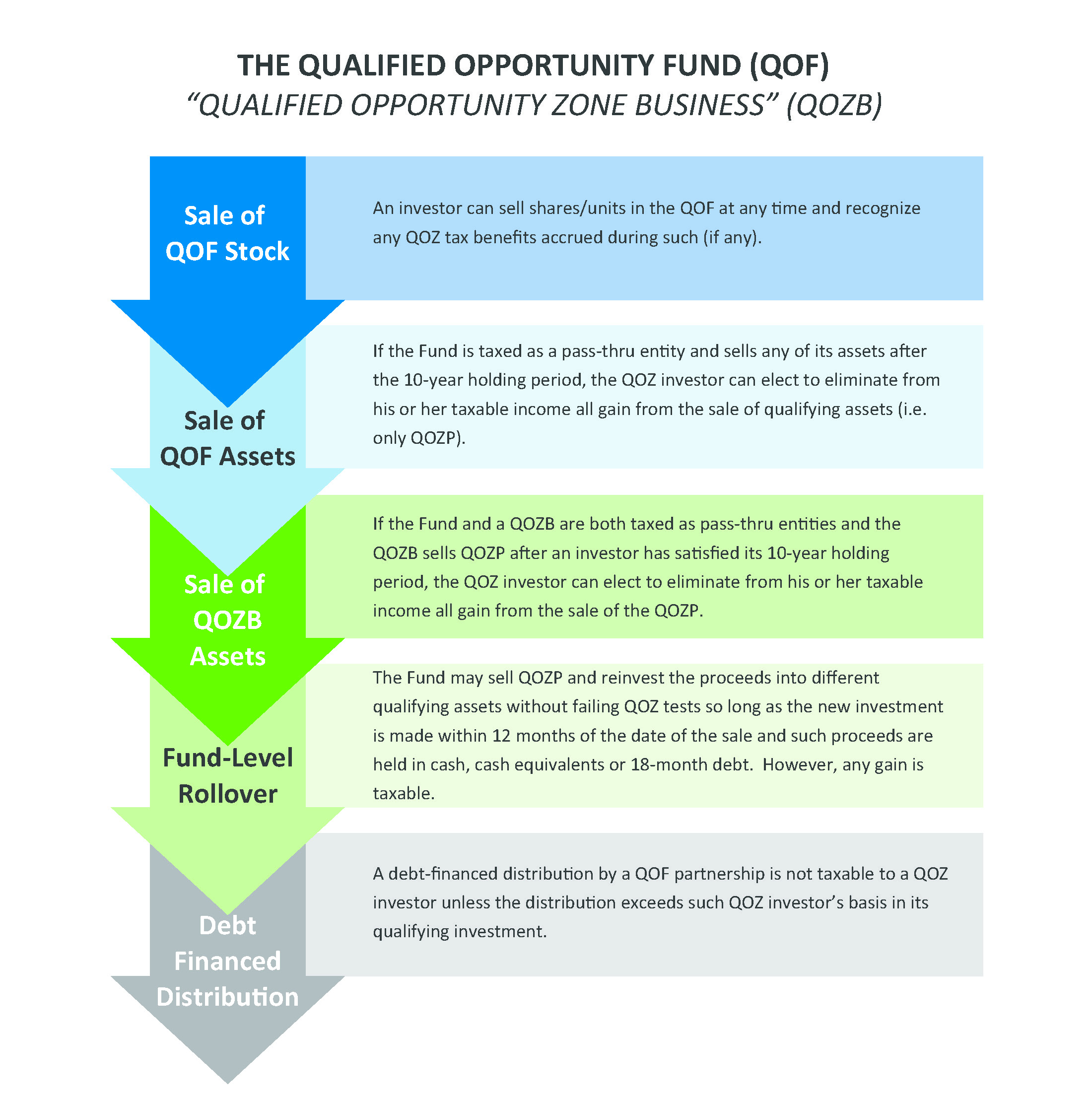

A Qualified Opportunity Fund (QOF) specializes in attracting investors with similar risk and reward profiles to collect and place capital in rural and low-income urban communities. Specific requirements of QOF’s include:

- Need to be funded by private capital and guided by market principals.

- Need to invest 90% of their assets in Opportunity Zone assets.

- May invest in Opportunity Zones via stock, partnership interests, or business property.

- Need to use assets to create new business activity.

- Need to double the investment basis over 30 months.

Requirements

70% of the business’ tangible property needs to be:

- Acquired after 2017 from an unrelated party,

- Used in any Opportunity Zone 70% or more of the time,

- Original use property or substantially improved.

A business needs to:

- Get 50% of its revenue from active conduct in any Opportunity Zone,

- Use 40% or more of its intangible property in any Opportunity Zone,

- Not hold non-qualified financial property beyond reasonable working capital,

- Operate in eligible business sectors (ineligible activities include: golf courses, country clubs, gambling establishments, among others outlined by Treasury regulations).

Business owners will also need to consider whether they are:

- Willing to give up equity in their business,

- Likely to grow significantly over the next 10 years,

- Likely to remain in a qualified Opportunity Zone for the next 10 years.